What happens when insurance companies decide to withdraw and no longer cover the most at-risk areas? That is the theme at the heart of the new report by the environmental NGO, but also of "Sigma", that of the Swiss Re Institute. Analysis

"Flexibility solutions are now essential. However, they face a structural difficulty: their costs are decreasing faster than market rules evolve," explains Xavier Blot, associate professor at emlyon business school.

By naming their first edition "Wind farms are taking shape", the industry's players want to show a certain optimism despite a context that remains complicated for the sector. A look by Benoist Guillard, president of the Groupe romand pour l’énergie éolienne (GREE).

"Instead of strengthening aid to cleantechs, Switzerland is doing the opposite."

Two months ago, CleantechAlps published the second edition of its report dedicated to start-ups active in the field of cleantech. Interview with Eric Plan, Secretary General.

Two months ago, CleantechAlps published the second edition of its report devoted to start-ups active in the cleantech field. More than 600 companies are now striving to reduce humanity’s impact on the planet, including around seventy highlighted in this study. Eric Plan, coordinator of this initiative, reveals to us the dynamics of an ecosystem in full transformation. Interview.

How did you select the start-ups featured in the report?

Since our main objective was to provide as representative a snapshot as possible and to offer a global view of this ecosystem, we made sure that the selected start-ups come from all sectors, from all regions of Switzerland and from different stages of maturity.

Our selection also focused on companies offering innovative solutions or shedding a different light on emerging sectors, often little identified as part of the cleantech domain.

Used everywhere, hasn’t the word “cleantech” become a catch-all term, emptied of meaning?

The problem with cleantechs lies in their positioning straddling several domains. Unlike the banking, oil or agri-food sectors, they do not constitute an industry branch in their own right. This cross-cutting nature can create that impression of fuzziness.

To dispel this feeling, we present a typology at the start of the study. Inspired by the segmentations proposed by the Cleantech Group and Roland Berger Strategy Consultants, we structured our panorama into seven major categories, themselves broken down into 22 subcategories.

How do you define cleantechs?

They encompass technologies, products and services designed for sustainable use of resources and the production of renewable energy. They aim in particular to reduce resource consumption and to preserve natural systems. This can include water, air, sand, rare earths, etc. Broadly speaking, they include all raw materials consumed by humans.

To define them, we were also inspired by the thinking of Gina Domanig, recognized as the most experienced cleantech investor in Switzerland. Founder of Emerald Technology Ventures, she describes cleantechs as “industrial technologies having a positive impact on the ecological footprint of one or more industry sectors.”

Moreover, the buzzword today is climatech, which incorporates the behavioral dimension of consumers, and no longer only technological innovations.

Cleantech, climatetech, greentech, eco-technology: what is the difference between these terms?

Each term has its own history, but all are synonymous, with more or less broad scopes. The term greentech, for example, is historical and dates back to the emergence of the sector in Silicon Valley in the mid-2000s. As for eco-technology, it is more a French term.

More broadly, cleantechs, or climatechs, denote solutions aimed at accelerating the transition from the old carbon-based world to a more sustainable society.

There are therefore relatively few failures in the cleantech field, compared with other sectors, such as biotech.

Seven years have passed between the first edition and the new one. What changes have you observed in the cleantech field?

By comparing the two editions, we note that among the roughly 600 companies founded between 2000 and 2023, the vast majority are still active. In total, only 10% of these companies are no longer operating under their trade names. Of that figure, we estimate that about a quarter of those disappearances are due to acquisition and the rest to bankruptcy. There are therefore relatively few failures in the cleantech field, compared with other sectors, such as biotech.

It is important to be transparent by specifying that, although the risk of bankruptcy is relatively low, the risk of betting on a future unicorn is also low. Cleantechs are not a sector in which one quickly generates enormous profits. Unicorns are rarer there because the need for investment, linked to the infrastructure required for deployment, is greater and takes more time than in sectors such as digital or pharma.

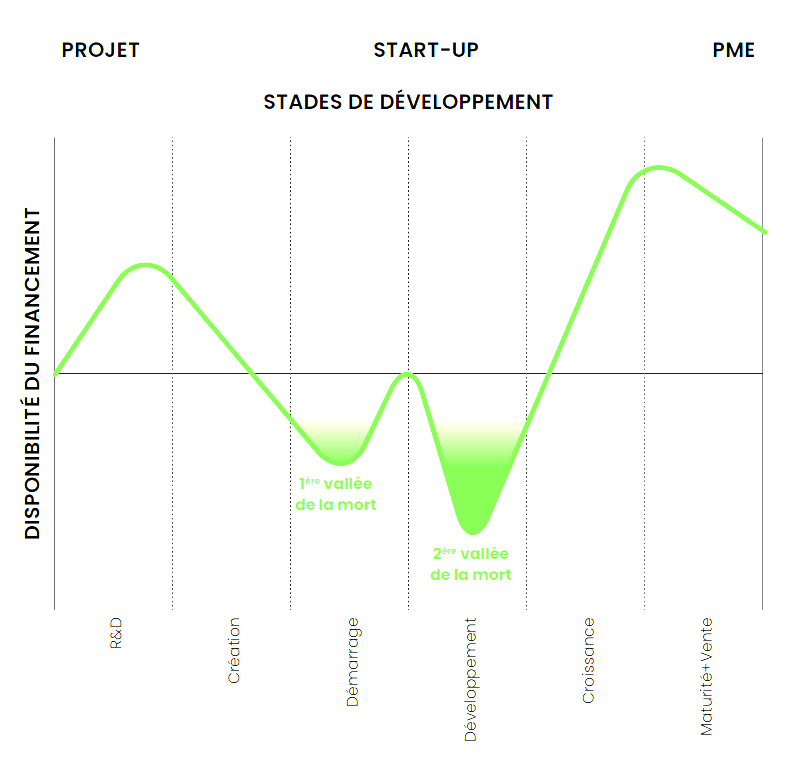

In the cleantech field, one speaks of a double valley of death...

This famous “valley of death,” the period when a start-up begins to operate but does not yet generate enough revenue to stabilize financially, indeed occurs twice. The journey of a company offering an innovation in sectors like energy, construction or chemistry is a real ordeal, which IT companies encounter less often.

The first occurs when the company must demonstrate the value of its technology in the field. The second is linked to the need to find the means to carry out pre-industrial pilots and then launch large-scale production. Indeed, in cleantechs, heavy infrastructure is often required to ensure product deployment. At this stage, we are talking about much larger funds to reach this objective. This requires investors to have “deep pockets,” patience and extensive industrialization experience.

This famous “valley of death,” the period when a startup begins to operate but does not yet generate enough revenue to stabilize financially, indeed occurs twice. @CleantechAlps

By comparing the cleantech sector with that of biotech, one can quickly perceive the particularities. The path of start-ups active in health is much more structured, with a preclinical phase, then a phase 1, a phase 2, etc. Investors know that funding needs will increase as the new molecule develops. If everything goes as planned, the return on investment can reach 1 to 2 billion. But if it fails, and this is very often the case, the loss is total.

For the cleantech sector, the risk is not only lower financially, but also in terms of success. Failures remain rare and, in the worst case, one ends up with an SME of 10 people that operates and allows, at least, partial recouping of the investment.

In 2022, the bursting of a bubble that had swollen during the Covid period brought the whole global cleantech industry to its knees. What were the consequences for the Swiss ecosystem?

First, it is important to emphasize that it was the entire venture capital sector that experienced difficulties. All start-ups, regardless of their sector, thus saw their investments slowed.

Did this situation discourage some investors and slow down the development of certain projects? The answer is complex, because 2022 was the year when Climeworks raised 600 million francs. Thanks to this considerable sum received by this company specialized in direct CO2 capture, investments in cleantechs in Switzerland reached records, despite the global market collapse. The aftershock was felt later, with a slowdown in investments in 2023 and 2024, a time span that is ultimately quite logical given that agreements take time to be concluded.

Like the rest of the economy, start-ups also suffered from the rise in central bank interest rates. The increase in the cost of money pushed investors to adopt a more cautious approach, favoring less risky assets that offer more attractive returns.

Although a global slowdown in investments has been observed for two years, the period remains favorable for company creation. Between 2011 and 2017, around thirty young shoots were born each year. Since 2017, this figure has increased to reach about fifty, which proves that the dynamic remains positive. For this year and the next, we expect to break new records, notably thanks to the new Climate and Innovation Act. Adopted in 2023, this law should provide financial aid to encourage the ecological transition and thus support the ecosystem.

The aftershock was felt later, with a slowdown in investments in 2023 and 2024, a time span that is ultimately quite logical given that agreements take time to be concluded.

The signals are therefore rather positive…

Yes, except that the Confederation is now considering significantly reducing its budget. Its cost-cutting program of 3 to 5 billion concerns many funds created to support the development of new technologies. Take, for example, the OFEN “Pilot and Demonstration” program. Although it sits at the interface between research and market, this program could, according to the results of the ongoing consultation, stop granting aid to applications submitted from 2027, or even from 2026.

The various funds created to support new technologies are currently being questioned. While it would be necessary to discuss how to strengthen support for clean energies and invest in the future, Switzerland is doing the opposite.

This situation is all the more absurd because by seeking to reduce its subsidy programs, the Confederation takes a considerable risk by exposing certain promising companies to the temptation to relocate abroad. In search of more favorable places for the development of new technologies, they could quickly be attracted by countries where it is not about repayable subsidies, but non-repayable grants.

Switzerland is therefore playing a dangerous game, threatening to break in a few months a positive dynamic that has lasted nearly two decades. Take the chemical industry, for example: this branch seems to be missing out on “sustainable chemistry,” a new major step but requiring costly infrastructure. Without public aid and without the possibility of co-financing its development, the whole sector risks missing this opportunity. Unfortunately, I am not convinced that this sector — an industrial flagship of the country for a century — is fully aware of the issues at stake in Bern, nor of the possible consequences for its future.

Federalism being what it is, all French-speaking cantons have put in place organizations or programs to support innovation, such as the Foundation The Ark, launched in 2004 in Valais. @CleantechAlps

What about the cantons, which all have programs or organizations to support innovation, like Innovaud? Is that sufficient?

Federalism being what it is, all French-speaking cantons have put in place organizations or programs to support innovation, such as the Foundation The Ark, launched in 2004 in Valais. Each of them follows its own dynamic and pursues specific objectives, linked to the canton’s strategic priorities and the composition of its economic fabric.

It is valuable to be able to rely on complementary actions at the cantonal level, because they are closer to the economic fabric than the Confederation and can therefore offer more targeted support. However, it is obvious that cantons should not, and cannot, substitute for national support to promote large-scale market deployment of innovations.

Switzerland prides itself on being at the top of the Global Innovation Index (GII) for several years. What is omitted is that this index, published each year by WIPO, is mainly based on patent statistics and does not take into account the ability to turn these inventions into real economic added value.

Let us recall that an innovation consists of a new way of doing something, generating economic value, that is, transforming an idea into a product with real commercial success. The realization of pre-industrial pilots is precisely the last development stage before scaling up to industrial level and ensuring wide deployment of products and installations. It is therefore essential to maintain, or even strengthen, co-financing instruments for market-ready projects.

Failing to do so would mean wasting public funds invested in research institutes (universities, EPF, HES), as many developments would not reach the market, or would end up in the hands of foreign actors who would exploit the results of this research… It is not only stupid, but it also shows a lack of vision and understanding of the product development phases, as well as the role of start-ups, which should be able to renew our economic fabric.

It is crucial that large industrial groups, the gas giants, as well as electricity producers and distributors, in turn learn to communicate better with start-ups and vice versa.

Could the solution come from the private sector?

Whether for cleantech start-ups or in other sectors, the problem of access to private funds remains constant. It is relatively easy to raise a few hundred thousand francs, or even a million, to start a project. However, a gap appears as soon as a start-up seeks to raise several million. Venture capital investors (VCs) are lacking in Switzerland, and this absence is even more felt in the cleantech sector.

Is it really necessary for these venture capital investors (VCs) to be based in Switzerland? I am not sure. In reality, the largest funds rarely invest in a single country. This is the case, for example, of Emerald Technology Ventures, the largest Swiss cleantech fund. According to its founder, Gina Domanig, this fund has invested in only three Swiss companies. The rest was invested in start-ups located in other countries.

Ultimately, the fact that Swiss start-ups finance themselves with European or international funds is not so problematic. Provided they are well informed about the local dynamics and have a presence in Switzerland to monitor its evolution, European investors can play a key role by highlighting the Swiss scene and creating a positive dynamic.

This dynamic is already manifested through Corporate Venture Capital, those funds that some multinationals allocate to invest in start-ups. These funds are booming because large companies have understood the interest of betting on new technologies. This is, for example, the case of the food industry giant Bühler with its recent innovation hub. By integrating young companies, it can thus access tomorrow’s technologies in advance. Oil companies are also adopting this strategy to anticipate the energy transition and the end of fossil fuels. It is crucial that large industrial groups, the gas giants, as well as electricity producers and distributors, in turn learn to communicate better with start-ups and vice versa.

What concrete actions do you recommend to support the ecosystem?

In 15 years, the sector has gone from an almost non-existent state to a network of more than 600 companies, with investments exceeding 3 billion, a large part of which was raised over the past five years. This impressive progression perfectly illustrates CleantechAlps’ vision, which, in 2010, defined three successive phases of about five years: emergence (2010-2015), consolidation (2015-2020) and finally, large-scale deployment (2020-2025+).

We have clearly passed the third phase, that of large-scale deployment. To date, this has mainly taken place on national territory, Switzerland acting as a pilot market. The next step for our young companies will be to expand internationally. The challenge ahead of them will be to prove their ability to cross Swiss borders, and for that, we will need significant co-financing to carry out pre-industrial installations, both in Switzerland and abroad.

I am speaking here not only of maintaining instruments such as pilot and demonstration programs, but also of doubling their funding to 50 million per year, by relaxing granting conditions, reducing analysis times and accepting a calculated risk-taking. Although these amounts are significant, they remain 10 to 100 times lower than those allocated to research… Do we want to retain a cutting-edge industrial activity in Switzerland, or be content to produce brains? That is clearly the stake of current discussions in Bern!

In the future, it will be essential to work with the banking and financial sector to propose instruments supporting the financing of products covering both CAPEX and OPEX. Although Swiss products are reputed for their high cost, they stand out for their quality, precision and longevity. The challenge is to help customers finance the purchase of solutions that, although costly at the outset, prove more profitable in the long run. We also speak of favoring low-tech innovations, born from frugal innovation logic, which aim for simple, robust, less expensive solutions, while being made with the attention to detail typical of Swiss quality.

It is becoming urgent to lift certain taboos and to share a common vision and values among all actors, in Switzerland and internationally. The cleantech sector suffers from a lack of synergy between domestic market actors and those responsible for international activities, which hinders its development. Without a global strategic approach, current growth risks losing its momentum, which would be a real waste.

The cleantech sector suffers from a lack of synergy between domestic market actors and those responsible for international activities, which hinders its development.

What is Switzerland’s international reputation in the cleantech field?

It would be an exaggeration to say that we excel in all areas, but Switzerland currently stands out in several sectors, such as agri-tech, waste valorization, the design of new materials, as well as energy efficiency associated with big data and AI. Among notable niches are photovoltaic inverters (which convert the solar energy from panels into electricity usable in homes) and water treatment.

If Switzerland has produced some SMEs that have gained worldwide renown, there is today no giant or locomotive comparable to those that have emerged in other countries. Contrary to Doris Leuthard’s promises in 2009-2010 with her Cleantech master plan, Switzerland is clearly not a leader in production, but it is more so in solutions.

These solutions are precisely those we should better sell and defend. This implies notably better integration between the different actors of the ecosystem. While it would be necessary to create more bridges between start-ups, scale-ups and large companies like Bobst or Stadler Rail, Switzerland tends to isolate them in silos. This reflects a regrettable lack of vision.

In the long term, this situation could harm our country which, while investing heavily in research and education, does not take the necessary measures to build a strong industry and consolidate its economy.

What will the Swiss cleantech ecosystem look like in a few years?

Cleantechs are solutions to move from a world based on fossil fuels to a decarbonized and sustainable world. Today, the portfolio of available cleantech solutions accompanies companies’ decarbonization trajectories.

The Swiss cleantech ecosystem will be strengthened with the field deployment of solutions, both in Switzerland and internationally. Its development speed will depend directly on political will and the legal framework, more or less restrictive, that will be put in place in the coming years. I am convinced that the transition will take place progressively, but that in 10 years, the cleantech ecosystem will no longer be a separate topic; it will have become the new benchmark.

And what will be the impact of AIs on the ecosystem?

AI is already very present in the cleantech ecosystem. Examining the distribution of the 600 cleantech start-ups, we find that one sixth of them are classified in the AI category. This number has multiplied by six over the past seven years and continues to accelerate.

This article has been automatically translated using AI. If you notice any errors, please don't hesitate to contact us.

What happens when insurance companies decide to withdraw and no longer cover the most at-risk areas? That is the theme at the heart of the new report by the environmental NGO, but also of "Sigma", that of the Swiss Re Institute. Analysis

"Flexibility solutions are now essential. However, they face a structural difficulty: their costs are decreasing faster than market rules evolve," explains Xavier Blot, associate professor at emlyon business school.

By naming their first edition "Wind farms are taking shape", the industry's players want to show a certain optimism despite a context that remains complicated for the sector. A look by Benoist Guillard, president of the Groupe romand pour l’énergie éolienne (GREE).

Since its founding in 2021, the young startup has made it its mission to find a good compromise between energy production and plant growth. The solution is called "spectral filtering".