What happens when insurance companies decide to withdraw and no longer cover the most at-risk areas? That is the theme at the heart of the new report by the environmental NGO, but also of "Sigma", that of the Swiss Re Institute. Analysis

"Flexibility solutions are now essential. However, they face a structural difficulty: their costs are decreasing faster than market rules evolve," explains Xavier Blot, associate professor at emlyon business school.

By naming their first edition "Wind farms are taking shape", the industry's players want to show a certain optimism despite a context that remains complicated for the sector. A look by Benoist Guillard, president of the Groupe romand pour l’énergie éolienne (GREE).

There is no paradox in sustainable finance also being synonymous with profitability.

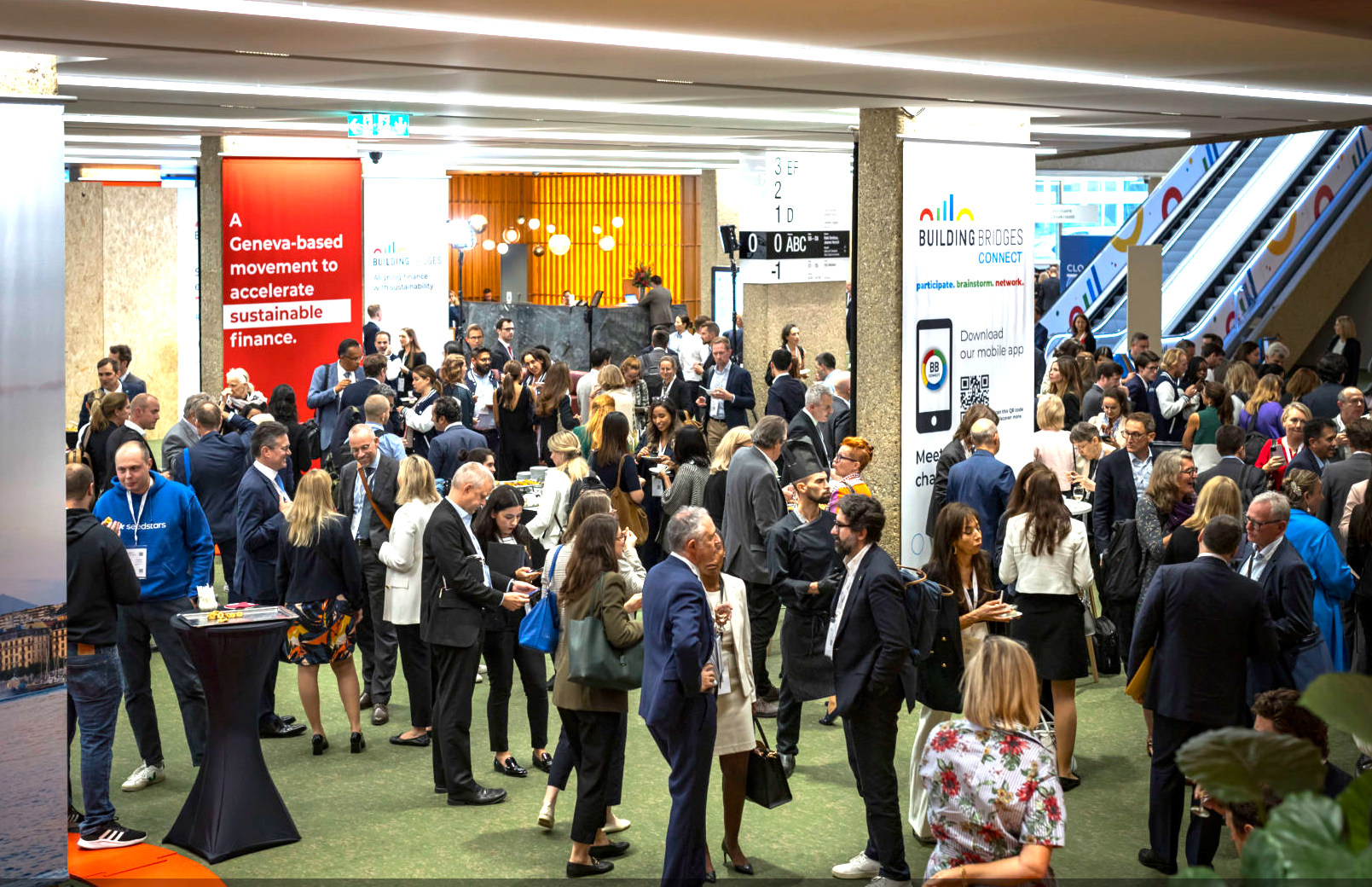

From December 9 to 12, Building Bridges will welcome participants from over a hundred countries. Interview with Patrick Odier, the president of the Geneva event.

Since its creation five years ago, Building Bridges has become an unmissable year-end event. From December 9 to 12, this Geneva event will welcome participants from more than a hundred countries. Private and financial sector actors, government members, academic experts and NGOs will gather to debate essential issues such as sustainable finance, valuing nature and biodiversity, the emerging role of AI, as well as a range of topics allowing a rethink of the financial system.

However, it is in a troubled context that this sustainable finance summit opens its doors. Paradoxically, while the financial sector keeps proclaiming its commitment to a greener economy, actions often contradict these fine words. Declines in sustainable investments, hedge funds betting against renewable energies, missed international meetings (COP29, biodiversity COP, plastics summit, etc.), the current winds rarely favor the planet.

It is in this context of promising and lively discussions that we met the president of Building Bridges, Patrick Odier. Interview.

Let's start by discussing the semi-failed finale of COP29. What is your analysis of what happened in Baku?

My first observation is that, once again, decisions were taken in a hurry at the end of the session. Certainly, the negotiations are complex, but this has been going on for quite some time already. Although the difficulties were known from the start, negotiators found themselves, two days before the closing, painfully trying to reach a compromise which, by definition, will not be fully satisfactory to either side.

My feeling regarding these COPs is that there is a problem with rhetoric. By constantly revisiting statements already made, they keep plunging back into old discussions instead of treating them as settled. This not only creates confusion, but also contributes to discrediting past decisions. Take fossil fuels for example: when states agreed in 2023 on an orderly phase-out, that was an important declaration. So why reopen the discussion on this subject and insist on their inability to reiterate this declaration? This kind of backtracking harms the process.

I wonder today whether the organization and format of these discussions have reached their limits, and whether it might be time to call into question the COP process. After all, these topics have been addressed in this framework 29 times, and results remain as hard to obtain. Meanwhile, the problems keep getting worse.

Isn't this difficulty in negotiations precisely linked to the worsening situation?

Absolutely. The severity of the challenges is increasing, both in scale and in pace. Expert reports are unequivocal: we are moving in the opposite direction to the goals set to address the major climate challenges. And as the time to act shrinks, the pressure only increases. This explains not only the complexity of the discussions, but also the growing tensions between actors.

Can we speak of a global distrust of environmental causes?

Let's put the results obtained in Baku into perspective. It is still an agreement of $300 billion, which is far from negligible. It's even three times more than previous promises. However, it will be crucial that these amounts really be made available to emerging countries, which suffer more from climate change than developed countries. Within what timeframe and in what form will these funds be disbursed? Will they be grants, loans, or a combination of both? Will they be conditional? Many uncertainties still hang over this financing, which I hope will be allocated more easily than the billions promised at previous COPs.

I am more concerned by the divide between Southern and Northern countries. This division is regrettable, because it is crucial to reach an agreement rather than oppose each other in the search for solutions. I remain convinced that states must play a central role in this transition. It is necessary to reach intergovernmental agreements to determine the amount and agenda of capital flows to be transferred from North to South. Such oversight is essential to ensure effective use of raised funds, because the international financial system alone cannot suffice.

On a more positive note, it should be emphasized that states have finally begun to discuss the creation of a global carbon market. Such a system would put an end to current disparities, where the price of a ton of carbon ranges from $100 in Singapore to five times that in Toronto.

"The topics addressed within Building Bridges will be influenced by international agendas and current geopolitical tensions. This edition will therefore be marked by the pressure of many headwinds."

In what state of mind are you starting this new edition of Building Bridges?

We know that this year is extraordinarily complex. The topics addressed within Building Bridges will be influenced by international agendas and current geopolitical tensions. This edition will therefore be marked by the pressure of many headwinds.

I am thinking in particular of the politicization of the debate on measures to safeguard the planet, as well as the fragmentation of public opinion on these issues. The involvement of a significant part of the population in this transition remains uncertain, due to a difficult economic situation. The impoverishment felt by many citizens has consequences that complicate the understanding of the urgencies, not to mention the impact on elections in some countries. The current evolution of the political landscape clearly does not send a favorable signal to achieve the goals set in Paris in 2015.

This complexity for 2024 also lies at the regulatory level, including in the financial sector. We are facing regulation made up of technical requirements and additional bureaucratic constraints, which also hinder initiatives in favor of a rapid transition.

Between the first edition of Building Bridges and that of 2024, do you feel that the situation has deteriorated?

I observe a certain fatigue. It is understandable given all that we have mentioned in terms of headwinds. The problem is that this weariness creates a risk of disinterest that must absolutely be countered. That is why Building Bridges strives to maintain an open and inclusive space for dialogue, capable of exploring new solutions adapted to current challenges.

Our main challenge will be to arrive at an agenda aligned with real priorities, while accelerating measures intended to facilitate a sustainable transition, including by the financial sector.

Biodiversity COP, COP29, world conference on plastics, Building Bridges in Davos in January… There are now many forums where environmental issues are discussed, but don't you find that, on the ground, concrete actions are still lacking?

For Building Bridges, this is a central question: what concrete objectives should we set during our key moments or our activities in general? I think we must aim for a change in mindset, on the one hand, and on the other, establish a common and strengthened language.

On the mindset front, the challenge is to remember that the transition will not happen in two or three years, but over a time horizon that is difficult to grasp, because it varies depending on situations and responsibilities at the time. We must therefore expect temporary deviations, the essential thing being not to lose sight of the final objective. Building Bridges strives to keep this course by reaffirming the goals to be achieved, the deadlines to be met and the policy choices to be considered.

"Our objective, in all modesty, is to bring all these forces together within Building Bridges and to advance the discussions a little more quickly."

What do you mean by "a common and strengthened language"?

It is essential, for the financial sector, to clarify the reasons why it is willing or not to engage in certain directions related to the sustainable transition. This would not only avoid a head-on opposition between the financial world and other sectors, but also help to establish a more coherent framework and timetable. The main objective of Building Bridges is to allow finance, through dialogue, to play a key role in accelerating this sustainable transition.

Isn't that one of Building Bridges' main challenges? Too many discussions and not enough concrete actions?

Building Bridges aims to bring to the same table civil society, NGOs, international organizations, as well as academic, industrial, financial and governmental sectors. Its main role is to create a dynamic that encourages this community to adopt concrete measures and move to action.

In terms of actions, we have contributed to the development of a roadmap for the Swiss financial industry, in collaboration with Swiss Sustainable Finance. This document provides valuable guidelines to help economic actors establish a constructive dialogue with the companies in which they invest, notably on environmental issues.

Another concrete action is the development of the "Swiss Climate Scores," an alternative methodology to the European taxonomy. Rather than rigidly classifying economic activities, as in Europe, Switzerland chose a more flexible and scientific approach. Launched in 2022, this optional method allows the sustainability of financial portfolios to be assessed and supports companies in their transition towards more responsible models.

Finally, within the framework of Building Bridges, we have sometimes exerted influence ahead of other major international conferences. This was the case with the dialogues in Sharm el-Sheikh preparatory to COP28, the second session of which was held under the aegis of Building Bridges. We also organized the post-COP15 conference, during which the United Nations presented new standards focused on nature conservation, beyond climate issues.

And this year, Building Bridges will organize a reference roundtable under the aegis of the United Nations. Biennial, this event will bring together nearly 500 professionals and negotiators over a day and a half.

Despite its youth, Building Bridges is beginning to enjoy an international aura and to carry more and more weight…

We undeniably respond to a growing need for dialogue and for gathering actors who already discuss the same topics in other frameworks, sometimes redundantly. Our objective, in all modesty, is to bring all these forces together within Building Bridges and to advance the discussions a little more quickly.

In recent weeks, we have learned of a worrying reality: finance remains distant from ecological goals. A study revealed that the world's largest hedge funds are betting against renewables while maintaining long-term investments in fossil fuels. What is your reaction to this situation?

It highlights a deeply rooted dilemma in finance: the tension between the short term and the long term. In the short term, some actors are remunerated to take advantage of market fluctuations, without worrying whether they favor renewables or not. This short-termism is an integral part of their business model. It also reflects the responsibility of financiers towards their clients: finding a balance between the risk profile they offer and the one their clients expect.

It is also crucial to emphasize another point: capital flows in favor of the sustainable transition are not limited to financing renewables. They also include investments in transforming large industries. It is now indisputable that sustainable development is not limited to a particular sector, but encompasses the whole economic activity.

A piece of good news is that, overall, the movement has been launched in most sectors. Today, the majority of economic actors are gradually becoming aware of the need to adapt their models and practices to face climate, environmental and societal challenges. These are factors that will need to be taken into account, otherwise the damages will be irreversible and will lead to additional tensions within our societies in the medium and long term.

"It is also crucial to emphasize another point: capital flows in favor of the sustainable transition are not limited to financing renewables."

Can the financial world really claim to be green within its current logic of profitability and performance?

In the short term, probably not, because the system pushes to support actors whose profitability is indeed crucial, but whose core activity is not truly sustainable. However, in the long term, we can only succeed in this transition effectively if finance becomes both sustainable and profitable. And I do not speak only of financial profitability.

The benefits of upcoming changes could, for example, translate into societal progress, such as improved social justice and protection of human and fundamental rights.

On the economic level, we must expect new paradigms, such as full transparency of supply chains for all the products we consume. Without this, companies risk finding themselves in extremely delicate positions, not only in front of politicians and regulators, but also with respect to their employees, who might refuse to work for them. A similar dilemma could arise for their shareholders, who might no longer wish to invest in companies that do not implement transparent and sustainable practices.

Thus, in my view, there is no paradox in the transition to sustainability also being synonymous with profitability.

Is there not, however, a need for the financial sector to sacrifice part of its profitability, linked to this short-term market vision, in favor of less profitable but promising long-term investments?

The transition must be global. It is not a question of opposing sustainable investments to others, but of ensuring that the medium-term trend remains positive, rather than focusing on short-term fluctuations.

Take the conflict in Ukraine: ten years ago, no one would have imagined a war breaking out in Europe. Today, we measure its consequences on global supply chains and on the energy sector. However, such events are not part of long-term economic and cyclical realities.

Although these events have short-term repercussions, it remains essential to ensure that measures taken in the medium and long term are appropriate, notably by ensuring continued investment in renewables. This also implies supporting technological innovations, such as those currently developing in the nuclear field.

Do you understand that this kind of news can harm the image you are trying to promote to the general public?

It is obvious that this highlights a crucial need for transparency. For the banking sector, this implies having a clear view of the global macroeconomic context in order to favor long-term sustainable investments. At Lombard Odier, for example, we are convinced that this transition represents the best source of profitability and opportunities for the portfolios we manage.

It is established that the energy transition and the achievement of the Paris goals will require colossal investments. In your opinion, are the banking and financial sectors doing enough to mobilize the funds necessary for this transition?

The financial sector cannot act alone; the entire private sector must be fully involved. Major economic and industrial players, holders of considerable resources, occupy a strategic position. Without their commitment, the transition will be unachievable.

If you ask me: "Can banks achieve it?", my answer is that the responsibility does not lie with banks alone, but with the entire financial sector. The question of risk is paramount. Without proper management of risk, no progress will be possible. That is why close collaboration with the public sector is indispensable. Technically, this takes the form of "blended finance," a mechanism where the private and public sectors partner to share both risks and opportunities.

"It is therefore perfectly logical that the bank does not play the role of a venture capital actor and that it does not engage directly in financing start-ups."

Switzerland is home to more than 600 start-ups, many of which are seeking financing. Isn't it time for banks to start investing in these young companies?

You touch here on an issue linked to venture capital and the evolution of the framework conditions in Switzerland. Currently, it is mainly specialized players who support this innovation ecosystem. In the process of creating companies, it is often observed that the resources needed for development phases are more easily accessible abroad. This situation is explained as much by Switzerland's small size and specificities as by hesitations in the local financial sector.

It would be incorrect to claim that banks do not wish to support company creation. However, they often favor other approaches, supporting already established players who generate demand opportunities and partnerships for start-ups. By contributing to maintaining Switzerland's position as a world leader in sectors such as food, chemicals-pharma and inspection, banks finance technological innovation, although this does not necessarily pass through direct support to start-ups.

That said, banks can also invest in young companies by allocating capital through funds specialized in venture capital. It is essential to emphasize that the venture capital profession differs from that of traditional banks.

Do you think Switzerland lacks public incentives to encourage banks to support start-ups more directly?

It is not for a bank to take, with its own funds, risks that exceed its essential mission: namely financing companies over the long term through loans or investments. The role of the bank is not that of a venture capitalist. Its mission is to lend funds to feed the economy where it needs it, to support the development of companies, to create jobs and foster the growth of a country. That is its primary mission.

Its second mission is to preserve savings: those of the employee, the future retiree, the investor, etc. These two functions are all the more justified or criticized depending on the level of risk they entail. It is therefore perfectly logical that the bank does not play the role of a venture capital actor and that it does not engage directly in financing start-ups.

What about green bonds? Should Switzerland continue down this path and, at the same time, reduce the risk for investors in this type of asset?

Green bonds represent a promising path that Switzerland should deepen, notably for public authorities. At the same time, it would be pertinent to develop sustainable bonds aimed at companies and local authorities, a concept that partially emerged during discussions at Building Bridges.

These instruments add a more civic dimension to finance. When a municipality or a canton issues a so-called sustainable bond to raise funds for projects that have a positive impact on society, the message becomes clearer and more understandable. For example, financing the strengthening of green spaces or sports infrastructure at the cantonal level will no doubt be better perceived by citizens than other forms of financing.

However, to promote this transition, it is crucial to establish a favorable framework that encourages public authorities to issue this type of instrument rather than others. This could be realized through more advantageous financial conditions, such as lower interest rates or reduced costs.

In this context, banks and asset managers have an essential role to play. They must continue to innovate and develop new financial instruments, in addition to those already existing, such as microcredit, impact investing, blended finance, or direct investment in funds dedicated to the climate transition.

"In just 30 years, we have transformed the way we produce energy, a change unprecedented in human history."

Returning to current events, how did you react to Donald Trump's return to the head of the American state?

His early statements about withdrawing the United States from certain international initiatives are certainly worrying, but will they actually materialize? It's still too early to say. Nevertheless, Trump's return to the White House should be seen as a worrying signal, likely to influence other actors who are still hesitant to invest in the energy and climate transition.

It is also important to recall that, in the American context, the energy transition does not depend exclusively on Washington. It also relies on a responsibility shared with the states, supported by the private sector. Many governors have already implemented policies favoring this transition and will continue to do so under Trump's presidency. His election could therefore prove less catastrophic than some fear.

It is somewhat ironic to note that some of the states most resistant to sustainable investments, often invoking dubious arguments against their fossil industries, are today among the largest producers of renewable energy in the country. Let us welcome the fact that the world's leading power is already, in many respects, engaged in this more responsible dynamic.

Current political developments in the West nevertheless seem to be evolving against green policies; how can we remain hopeful?

It is possible to remain optimistic for two reasons. The first lies in the fact that we are crossing a crucial threshold between yesterday's world and the sustainable world of tomorrow. Certainly, progress varies by region, but notable advances are visible. For my part, I observe it through the companies with which we collaborate: all have reorganized their executive management to integrate sustainability into their strategy.

Are these efforts fast enough? Probably not, but the pace of this transition cannot be dissociated from the economic and social realities in which it unfolds. One must also take into account the collateral effects associated with these changes. Take the example of palm oil exploitation: it is easy to say "I would like to stop, but what can I do instead and with what financial means?" This type of challenge is complex to resolve and will require adapting the speed of the transition according to local contexts.

One last positive point to mention: the extent of the path already traveled. What we have achieved in terms of innovation in energy production is historic. In just 30 years, we have transformed the way we produce energy, a change unprecedented in human history. This transition to solar and wind energy represents the most significant model transformation in all of human history. We have initiated a major revolution, and it is crucial that it be recognized and celebrated.

This article has been automatically translated using AI. If you notice any errors, please don't hesitate to contact us.

What happens when insurance companies decide to withdraw and no longer cover the most at-risk areas? That is the theme at the heart of the new report by the environmental NGO, but also of "Sigma", that of the Swiss Re Institute. Analysis

"Flexibility solutions are now essential. However, they face a structural difficulty: their costs are decreasing faster than market rules evolve," explains Xavier Blot, associate professor at emlyon business school.

By naming their first edition "Wind farms are taking shape", the industry's players want to show a certain optimism despite a context that remains complicated for the sector. A look by Benoist Guillard, president of the Groupe romand pour l’énergie éolienne (GREE).

Since its founding in 2021, the young startup has made it its mission to find a good compromise between energy production and plant growth. The solution is called "spectral filtering".