What happens when insurance companies decide to withdraw and no longer cover the most at-risk areas? That is the theme at the heart of the new report by the environmental NGO, but also of "Sigma", that of the Swiss Re Institute. Analysis

"Flexibility solutions are now essential. However, they face a structural difficulty: their costs are decreasing faster than market rules evolve," explains Xavier Blot, associate professor at emlyon business school.

By naming their first edition "Wind farms are taking shape", the industry's players want to show a certain optimism despite a context that remains complicated for the sector. A look by Benoist Guillard, president of the Groupe romand pour l’énergie éolienne (GREE).

When climate change tends to make the world uninsurable

What happens when insurance companies decide to withdraw and no longer cover the most at-risk areas? That is the theme at the heart of the new report by the environmental NGO, but also of "Sigma", that of the Swiss Re Institute. Analysis

“Insurance is one of the pillars of modern prosperity.” As the introduction to one of WWF’s latest studies, this short sentence sums up one of the major problems of our time: what happens when that option no longer exists? What becomes of things when insurance companies decide to withdraw and stop covering the highest-risk areas? That is the theme at the heart of the environmental NGO’s new report, but also of “Sigma,” the Swiss Re Institute’s report.

“Climate change and the destruction of protected natural areas are making whole regions increasingly difficult to insure and are depriving millions of people of protection against climate disasters. This has considerable social, economic and financial consequences,” warns Jérôme Crugnola-Humbert, co-author of the WWF report and an independent specialist in sustainable finance.

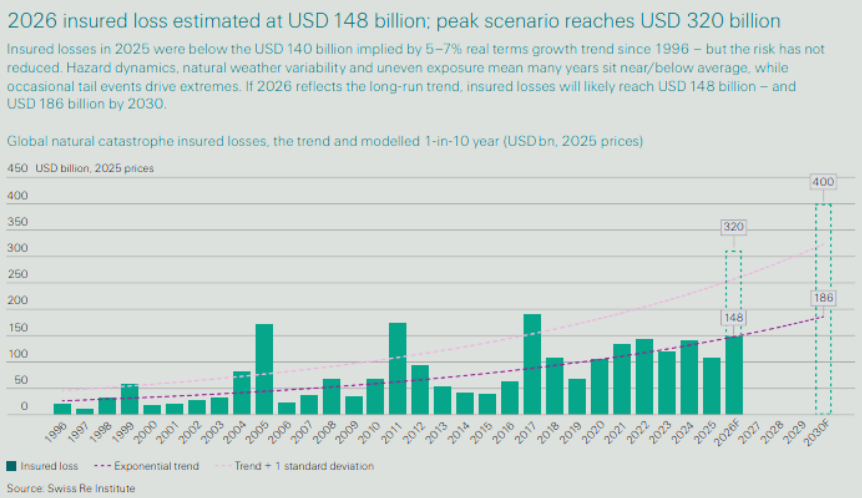

Although the latest estimates by Swiss Re experts present a moderate picture, with $107 billion in insured losses in 2025, the underlying trend is structurally upward, by 5 to 7% per year. For the current year, early projections range between $148 and $300 billion in the most extreme scenarios. Since some points overlap between the two studies, we offer you here a cross-summary in a few key points.

For the current year, early projections range between $148 and $300 billion in the most extreme scenarios. @Swiss Re Institute

1️⃣

A growing protection gap: Both reports sound the alarm about the same “protection gap,” the difference between economic losses caused by natural disasters and the portion covered by insurance. Each year, tens of billions of euros in losses go uninsured worldwide. “According to Gallagher Re, an international reinsurance broker, the global protection gap for natural disasters (including earthquakes, volcanic activity and extreme weather events) amounted to 63% in 2024 — which means that only about one third of economic losses were insured,” states the WWF report.

If these insurance protection deficits are growing worldwide, the situation is even more alarming in emerging economies, where 80 to 90% of disaster-related losses are not insured. “These gaps are explained by demand-related factors — such as low risk perception and the complexity of insurance products — as well as supply-related factors, like adverse selection and legal and regulatory constraints,” explain Swiss Re experts.

Such an insurance protection gap has significant macroeconomic consequences that are too often underestimated. Rising inflation, reduced household resources, a drag on investment, unaffordable housing, commercial and financial disruptions, and other contagion effects are among the many indirect risks. “These tipping points can trigger non-linear and self-reinforcing dynamics of asset devaluation, insurance losses and credit defaults, leading to a rapid rise in systemic risk on time horizons that are too short to allow for effective adaptation measures,” the WWF notes.

Each year, tens of billions of euros in losses go uninsured worldwide. @WWF

2️⃣

The weight of secondary perils: Historically, insurers and actuaries have relied on a vast amount of historical data to properly assess risks and reliably forecast potential future losses. The rapid mutation of the climate is disrupting this predictive model. “This mismatch of approaches is leading insurers to revise their pricing and capital models, as well as to reduce their underwriting appetite,” say the specialists at Swiss Re.

In this global dynamic, so-called secondary perils are the main troublemakers. Taking the form of small storms, floods (excluding those linked to tropical cyclones) or wildfires, these smaller but cumulative — and therefore costly — risks account for a large share of losses recorded since 1970. “Their intensification generates losses that far exceed economic growth, putting increased pressure on economies and the insurance sector,” emphasizes the Sigma report.

3️⃣

The importance of prevention: “Many regions of the world remain insufficiently prepared due to structural vulnerabilities, inadequate early warning systems and rapid, uncontrolled urbanization,” say Swiss Re experts. They are categorical: implementing adaptation and mitigation measures is essential to reduce the potential for losses and maintain insurability in exposed regions.

“Our analyses show that adaptation can significantly offset loss growth when implemented effectively. Flood protection measures — such as dams, dikes, retention systems and improved water management — prove particularly cost-effective,” they write.

The European case is especially instructive. In countries like the UK, France, Switzerland and Austria, research indicates that adaptation measures have reduced economic flood losses by around 63% since 1950, largely offsetting the increased risk linked to hazard intensification and the expansion of flood-prone areas. Sustainable, targeted investments in prevention therefore prove essential to avoid an acceleration of future losses.

WWF also recalls that it will be necessary “to fundamentally transform the management of our ecosystems and natural resources.” @WWF

4️⃣

Nature’s protective role:In its report, WWF emphasizes the importance of restoring nature’s role not only to mitigate the consequences of climate change but also to adapt to it. Investing in preventive measures, notably through solutions such as restoring forests or wetlands, proves particularly effective and cost-efficient. “Reducing pressures on ecosystems and restoring them is a cost-effective strategy to decrease vulnerability to extreme weather events as well as their intensity — provided this is carried out alongside efforts to mitigate climate change,” the NGO specifies.

To illustrate their point, WWF experts cite the particular case of forests. Located on slopes or in exposed areas, they act as barriers and buffer zones, reducing the probability and intensity of hydrological, gravitational or wind-related phenomena such as avalanches, landslides, floods or erosion. “The more resilient these forests are, the greater their capacity to reduce potential losses,” they assert.

The NGO also relies on the emblematic example of Switzerland, where the contribution to the management of protective forests amounts to about 5,000 francs per hectare per year (or 40% of net costs), the remainder being financed by the cantons, municipalities and private actors. WWF further points out that in Switzerland, “forests are already integrated into the risk management models used by public authorities and that some companies, such as insurer Helvetia, actively invest in their preservation, notably through targeted reforestation projects.”

“To secure our long-term prosperity, it is necessary to implement a coordinated strategy combining emissions reduction, nature protection and the development of new insurance solutions,” summarizes Jérôme Crugnola-Humbert, co-author of the WWF report and an independent specialist in sustainable finance.

In the future, given the growing risks related to climate disasters, it will indeed be necessary to rethink public policies and financial systems by jointly integrating climate, environmental and insurance issues. This approach calls for better accounting for the value of our ecosystems in risk assessment, encouraging prevention strategies and adapting regulation accordingly, while continuing to reduce greenhouse gas emissions.

WWF also recalls that nature itself will have to “adapt to climate change” and that it will be necessary “to fundamentally transform the management of our ecosystems and natural resources.” The NGO considers it essential that climate scenarios be integrated into the management of protected areas and landscapes, and that governments adopt policies that prioritize ecosystem resilience.

This article has been automatically translated using AI. If you notice any errors, please don't hesitate to contact us.

"Flexibility solutions are now essential. However, they face a structural difficulty: their costs are decreasing faster than market rules evolve," explains Xavier Blot, associate professor at emlyon business school.

By naming their first edition "Wind farms are taking shape", the industry's players want to show a certain optimism despite a context that remains complicated for the sector. A look by Benoist Guillard, president of the Groupe romand pour l’énergie éolienne (GREE).

Since its founding in 2021, the young startup has made it its mission to find a good compromise between energy production and plant growth. The solution is called "spectral filtering".

"Despite expectations, substantive discussions could not begin for lack of operational arrangements for the panel. Moreover, in the absence of a dedicated international body, the regulation of pollutants remains fragmented," worries Henri Klunge, chemical engineer and founder of Alcane Conseils.